There is a common myth, held especially among left-wing people, that post-war tax policy, with its high top marginal rates on labor income, was very punitive towards rich people, and because of that, it's one of the primary factors that drove the booming economy of the time. Justifications for such high marginal tax rates (70-94% in 1945-1980) vary. Some believe this is supposed to raise tax revenues, while others that it is supposed to reduce inequality, set an effective ceiling on earnings, and encourage employers to invest money in the company or employees rather than paying themselves and executives high salaries. However, there is no firm evidence that these rates served any of these purposes well in the post-war years.

Effective tax rates

First, it is important to note the difference between marginal tax rates and effective taxation. While personal income tax rates during the post-war era may suggest that the wealthy paid exorbitantly high taxes, in reality, the effective taxation of the wealthiest taxpayers was estimated to be comparable, marginally higher, or lower than today. Let's look at couple of these estimates. According to Piketty, Saez and Zucman paper from 2018 average effective tax rates paid by the top 1% in post-war period (1945-1973) fluctuated between 35-45%, with an average of approximately 40%. Although this rate is slightly higher than that of the post-1980s era (which ranged from 30-40%, with an average of around 35%), it's not a drastic difference.

Now, some economists disagree with their assumptions and estimates, and have produced their own approximations. Probably the most famous estimates (other than PSZ) come from the work of Gerald Auten and David Splinter. Their findings from 2022 paper suggest than top 1% faced an average tax rate of 35-40% in the 1960s (unfortunately their data starts in 1960), which was similar to post-1980s period (or even a little bit lower).

They also include more detailed measures of tax progressivety for some years, including average tax rates for top 0,1% and top 0,01%. According to their calculations, these groups faced higher effective tax rates in 2000 (exceeding 50%) and in 2019 (approximately 45%) compared to 1962 (between 40-45%).

Another estimate can be found on Tax Policy Center website. Their analysis is less sophisticated than PSZ or AS (doesn't include a lot of taxes, presents only 8 data points, and is based on much simpler assumptions), but it also shows no drastic changes in effective tax rates on the rich from 1955 (although somewhat larger changes for top 0,01% than for top 1%). The really big change seems to only occur at the beginning of the post-war period.

Regardless of the estimate, the rich didn't seem to face much higher effective tax rates during most of the post-war period (1945-1973) compared to the post-1980s era.

Why didn't the rich pay much higher taxes?

There are a few reasons why the effective tax rate of the wealthy was significantly lower than the marginal tax rates during that era. The first reason is that the highest tax rates were imposed on incomes that exceeded very high thresholds (usually over $200,000 for single filers, which would equate to $1.6-2.6 million in today's dollars), which affected only a small number of taxpayers. For example in 1963 only 501 taxpayers were subject to top 91% tax rate.

Some people might believe that the reason for this was that there were very few rich people during that time and count this as a success of post-war tax policy. But it is not entirely true. You can even find it in the IRS report linked above. There were a lot of people with incomes well above 200 thousands that weren’t subjected to this tax rate. Tax Policy Center (download Excel for historic data) calculated effective tax rates for different income groups based on the IRS data for selected years. Based on their calculations, in 1955 people with incomes over 1 million dollars (way over 200 thousand top marginal rate threshold and would equate to around 11 million in today's dollars) faced only 35,81% effective tax rate.

In 1965, effective tax rate for this group was even lower. While the top marginal rate was 70%, effective tax rate for people with incomes over 1 million dollars was only 26,66%.

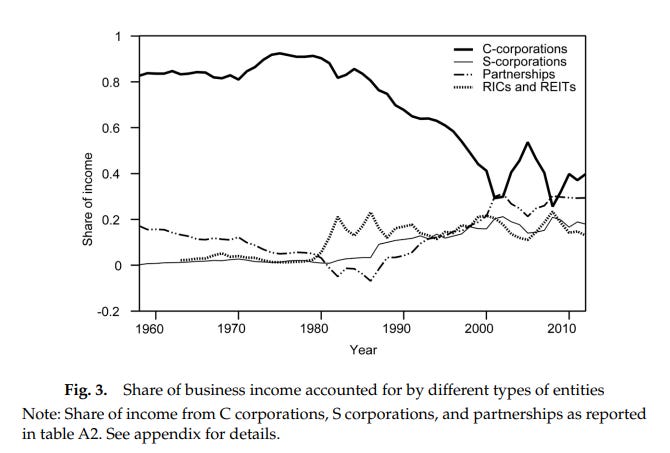

And one study from 1975 found that effective individual tax rate for millionaires in 1966 was around 20%. The reason for this is that the tax system in place created strong incentives to divert your income away from “labor income” towards other forms of income, that were taxed at lower rates. And there were many ways under the post-war tax code to do that. One way was to shelter your income inside corporations. Before Tax Reform Act (TRA) of 1986 top corporate tax rate was significantly lower than top marginal tax rate, which incentivized the rich to use corporations to defer individual taxes. We can clearly see this in the data. Number of C corporations (subject to corporate income tax) declined substantially following the introduction of TRA 86, while the number of S corporations (pass-through businesses, subject to personal income tax) rose.

Share of business income accounted for by different entities show a similar thing - sharp drop in C corporation share of income in the 80s and the rise of pass-through share of business income.

We can also see this on the Auten-Splinter graph above (second graph in this article). Corporate tax accounted for a much larger share of total taxation of the top 1% in the 1960s compared to now.

Sheltering income inside corporations was just one way of lowering the tax burden. Another optimization strategy involved using various loopholes to classify your income into capital gains. First thing we need to notice is that the capital share of income (that is share of income that is derived from capital and subject to capital gains tax) among the very rich was much higher during the post-war period compared to the post-1980s period. According to PSZ (2018) capital share of income for the top 0,1% was around 80% in the late 40s and early 50s, then jumped to around 90% in the late 50s and early 60s, dropped below 80% in the 70s and stayed below 70% post-1980s. For the top 1%, the share was around 70% for most of the post-war period and under 60% for most of the post-1980s period.

Capital income tax rate at that time was around 25% (or rather 50% paid on 50% of capital gains), much lower than the top marginal tax rates on ordinary income. Wealthy individuals went to great lengths to redirect their income toward the more favorable capital gains tax system. One way to do it was through the use of “collapsible” corporations, where an individual or a group would establish a company to acquire or produce a single asset. Before the realization of income, shareholders would sell their shares or dissolve the corporation, thereby converting a considerable portion of the ordinary income generated at the corporate level into long-term capital gain. This method initially gained popularity in the motionf picture industry, but it was quickly embraced by the real estate industry as well. IRS and the government tried to limit this tax avoidance scheme many times (especially with Section 341 of the 1954 Internal Revenue Code) but with little success.

Wealthy people used many other methods to exploit nuances of the tax code for favorable tax treatment. Conversion of personal service income to capital gains was elevated to an art form. Notable examples of this can include Jack Benny, who succesfully clasified his income from a contract with CBS as capital gains or president Dwight Eisenhower, who managed to clasify his income from selling the book “Crusade in Europe” as capital gains Treasury Department ruled that by not being a professional writer he rather marketed lifetime asset of his experience.

Another tax avoidance strategy was to take advantage of oil depletion allowances, which enabled oil companies to lower their taxable income by 27.5%. This allowance was widely embraced by Hollywood celebrities, who made substantial investments in the oil industry. Bill Crosby was likely the first movie star to use this tax scheme, but many others quickly followed suit, including Frank Sinatra, Jimmy Stewart, and Gene Autry. There existed numerous other methods to avoid taxes, such as taking advantage of favorable real estate depreciation rules (which some argue stimulated the post-war shopping-center boom), investing money into tax-exempt bonds, or utilizing tax-saving charitable deductions.

The widespread tax avoidance of the rich was common knowledge during that era. In 1968, Robert F. Kennedy, a New York Senator and one of candidates for the Democratic presidential nomination, brought attention to the numerous loopholes present in the tax law, which allowed wealthy individuals to evade their tax obligations. He proposed the implementation of a minimum tax rate for individuals with an income of over 50 thousand dollars, irrespective of the source of their earnings. The next year then Treasury Secretary Joseph W. Barr testified before Congress that in 1966, 155 taxpayers with incomes over 200 thousand dollars (currently about 1,9 million) paid no federal income tax at all. This revelation led Congress to implement a comprehensive series of reforms under the Tax Reform Act of 1969. These reforms included the introduction of new add-on taxes for both individual and corporate taxpayers, at a minimum of 10 percent on specific tax preferences, aimed at generating additional revenue from affluent taxpayers who had significantly reduced their tax liabilities through various tax shelters and preferences. They also included the limitation of specific loopholes and an increase in the capital gains tax rate.

Conclusion

The tax code in place affects the behavior and responses of taxpayers. To fully understand the tax systems of different periods and their implications, we need to look beyond the tax rates and analyze the incentives created by these rules. Despite popular claims, the post-war tax system did not substantially limit the incomes of the rich. Many loopholes allowed them to significantly lower their tax burden. If someone wants to "soak the rich" and reduce inequality, perhaps they should look elsewhere.